Habib Rice Products Limited (PSX: HRPL) was incorporated in Pakistan in 1980. The principal activity of the company is the production of rice-based starch sugar and proteins.

Pattern of Shareholding

As of June 30, 2024, HRPL has a total of 40 million shares outstanding which are held by 2259 shareholders. Directors, CEO, their spouses, and minor children have a major stake of 64.81 percent in the company, followed by individuals holding 17.92 percent shares. Associated companies, undertaking, and related parties account for 14.56 percent of shares of HRPL while Insurance companies hold 1.38 percent of shares of HRPL. The remaining ownership is distributed among other categories of shareholders.

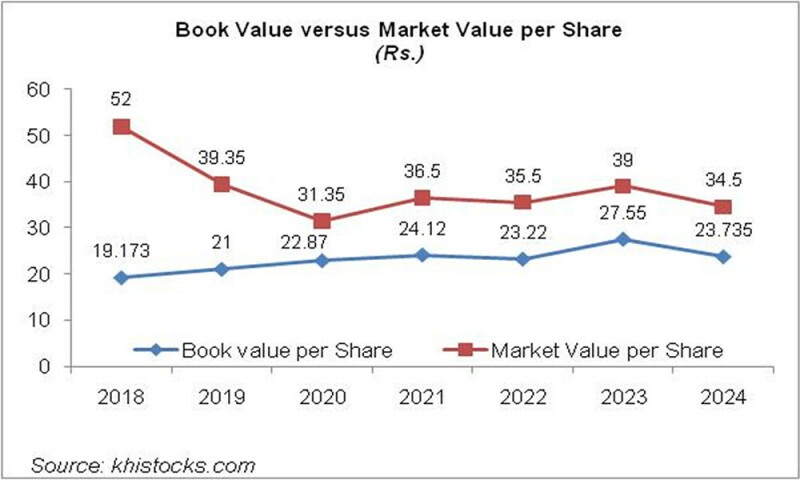

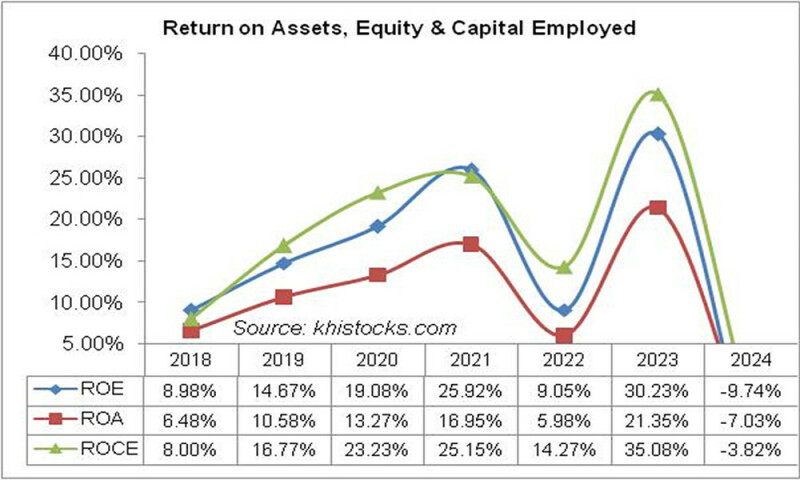

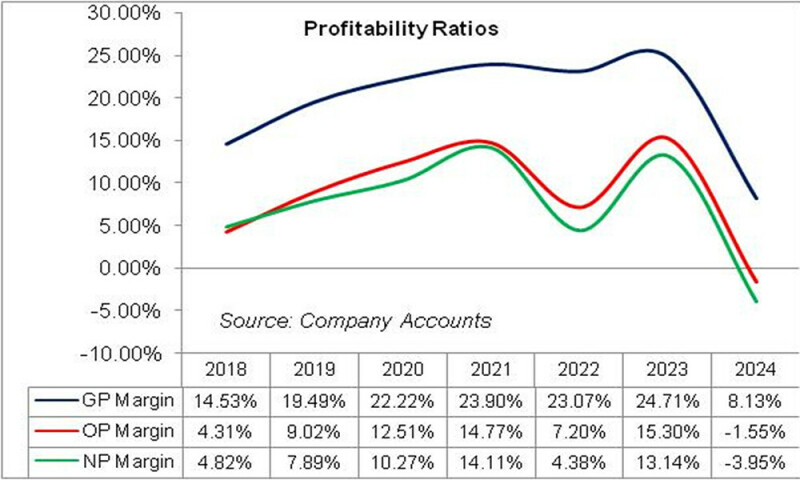

Financial Performance (2019-24)

HRPL’s topline has been riding an upward trajectory since 2019 except for a dip in 2024. Its bottom line slid in 2022 and 2024. In 2024, the company registered operating and net losses. HRPL’s margins went uphill until 2021 followed by a sizeable drop in 2022. In the subsequent year, the margins considerably recovered. HRPL’s margins posted their lowest levels in 2024. The detailed performance review of the period under consideration is given below.

In 2019, HRPL’s topline grew by 9.27 percent year-on-year. While local sales slumped on account of the dumping of sorbitol from India, robust demand for the company’s products in the export market drove the net sales up. The share of export sales in HRPL’s net sales grew from 13 percent in 2018 to 30 percent in 2019. Gross profit rebounded by a massive 46.58 percent year-on-year in 2019 as export sales provided healthy margins amid Pak Rupee depreciation. GP margin grew from 14.53 percent in 2018 to 19.5 percent in 2019. Higher export sales volume also resulted in elevated freight and commission charges, culminating in a 28.67 percent spike in distribution charges in 2019. Administrative expenses also inched up by 6.7 percent year-on-year in 2019 on account of higher payroll expenses incurred during the year. HRPL’s net other income rose by 55 percent year-on-year in 2019 due to higher profits from TDR and bank deposits as well as exchange gains. Operating profit multiplied by 128.53 percent year-on-year in 2019 translated into an OP margin of 9 percent, up from an OP margin of 4.3 percent recorded in 2018. Finance cost surged by 160.82 percent year-on-year in 2019, however, it only comprised of bank charges and commissions as HRPL didn’t have any external borrowings on its books. Net profit spiraled by 78.93 percent year-on-year in 2019 to clock in at Rs.123.25 million with EPS of Rs.3.08, up from EPS of Rs.1.72 recorded in 2018. NP margin also ascended from 4.82 percent in 2018 to 7.89 percent in 2019.

HRPL’s topline grew by 8.73 percent in 2020. The outbreak of COVID-19 and the associated restrictions on the movement of goods and people across borders resulted in a complete halt of sorbitol import from India. This created a supply gap in the market, allowing the company to increase its prices. HRPL’s export sales also slipped in 2020 on account of COVID-19, however, improved prices in the home market pushed the gross profit up by 24 percent year-on-year with GP margin picking up to 22.22 percent. Distribution expenses grew by 4.94 percent year-on-year in 2020 on the back of higher freight expenses and advertisement expenses. Higher payroll expense and depreciation on right-of-use assets drove up the administrative expense by 3.4 percent year-on-year in 2020. Net other income rebounded by 30.94 percent year-on-year in 2020 on account of splendid interest income on short-term investment. As a consequence, operating profit widened by 50.88 percent year-on-year in 2020 with OP margin jumping up to 12.51 percent. Finance cost surged by 34.30 percent year-on-year in 2020 due to accretion of interest on lease liabilities. Net profit rose by 41.6 percent year-on-year in 2020 to clock in at Rs.174.52 million, translating into EPS of Rs.4.36 and NP margin of 10.27 percent.

In 2021, HRPL’s topline posted a marginal 4.31 percent year-on-year growth due to lower sales volume as imports from India resumed during the year. However, better margins on export sales saved HRPL’s topline from falling. Gross profit picked up by 12.19 percent year-on-year in 2021 on account of higher margins on export sales. GP margin jumped up to 23.9 percent in 2021. Administrative expenses largely stayed at the same level as of 2020. Conversely, distribution expenses magnified by 25.95 percent year-on-year in 2021 as freight charges soared due to higher export sales. Net other income shrank by 12.61 percent year-on-year in 2021 due to lower profit on saving accounts and deposit receipts on account of monetary easing during the year. Operating profit picked up by 23.15 percent year-on-year in 2021 with OP margin rising up to 14.77 percent. Finance cost multiplied by 156 percent year-on-year in 2021 due to the unwinding of finance cost on provision for GIDC. Tax expense narrowed down by 94.96 percent year-on-year in 2021 on account of the tax credit from the prior year. This resulted in 43.26 percent year-on-year growth in net profit which clocked in at Rs.250.02 million with EPS of Rs.6.25 and NP margin of 14.11 percent.

HRPL’s net sales grew by 8.32 percent year-on-year in 2022. The non-availability of energy during the year resulted in curtailed plant operations which culminated in lower sales volume. Topline growth was primarily the result of higher export sales which constituted 33.5 percent of HRPL’s cumulative net sales in 2022 versus its share of 16 percent recorded in 2021. The high cost of energy coupled with an unparalleled level of inflation pumped up the cost of sales by 9.5 percent year-on-year in 2022. Gross profit grew by 4.55 percent year-on-year in 2022, however, GP margin slightly tumbled to 23.1 percent. Distribution expense surged by 87.66 percent year-on-year in 2022 on account of higher freight charges which was primarily the effect of elevated prices of POL products. The administrative expenses also multiplied by 18.22 percent year-on-year in 2022 due to higher payroll expenses as well as traveling & conveyance charges. Net other income tapered off by 44.28 percent year-on-year in 2022 due to higher unrealized loss on listed equity securities and lower profit on TDRs. Resultantly, operating profit shrank by 47.21 percent year-on-year in 2022 with OP margin falling down to 7.2 percent. To make things even worse, finance cost soared by 62.22 percent year-on-year in 2023 on account of higher unwinding of finance cost on provision for GIDC. Net profit contracted by 66.37 percent year-on-year in 2022 to clock in at Rs.84.08 million with EPS of Rs.2.10 and NP margin of 4.38 percent.

Among all the years under consideration, HRPL posted the highest year-on-year growth of 32 percent in its topline in 2023. Import restrictions forced the company to source its raw materials locally. This coupled with erratic gas supplies didn’t allow the company to operate at its optimum capacity. Hence, it liquidated its long-accumulated inventory in 2023. Cost of sales grew by 29.20 percent year-on-year in 2023 resulting in 41.36 percent higher gross profit and GP margin touching its highest level of 24.71 percent in 2023. Distribution and administrative expenses declined by 30.44 percent and 2.6 percent respectively in 2023 due to lower freight charges and payroll expenses respectively. Net other income further slid by 0.55 percent due to higher provisions for WWF and WPPF in 2022. Gain on re-measurement of GIDC grew by 23.95 percent in 2023 which buttressed the operating results. As a result, operating profit posted a staggering 180.62 percent rise in 2023 with OP margin climbing up to 15.3 percent. Finance cost grew by 8.71 percent year-on-year in 2023 due to higher unwinding of finance cost on provision for GIDC. Net profit showed a massive improvement of 296.11 percent year-on-year in 2023 to clock in at Rs.333.06 million with an NP margin of 13.14 percent and EPS of Rs.8.33.

In 2024, HRPL’s net sales dropped by 7.64 percent year-on-year. During the year, India imposed a ban on its rice export which drove the international prices quite up. In order to take advantage of the opportunity, Pakistani farmers quickly harvested the crop which still had moisture. To avoid fungal infection, the farmers used fungicide and held down alfatoxin which made the local crop non-organic and hence un-exportable. Resultantly, the local market was flooded with cheap soybean meal. This rendered HRPL’s protein unattractive, leaving behind unsold piles of inventory. Cost of sales mounted by 12.69 percent in 2024 due to higher prices of raw & packaging materials consumed during the year coupled with elevated utility charges. The unavailability of natural gas forced the company to continue its operations using expensive furnace oil and KE power. This resulted in a 69.59 percent decline in gross profit in 2024 with GP margin falling down to its lowest level of 8.13 percent. Distribution expenses mounted by 17.47 percent in 2024 due to a hefty advertisement & promotion budget coupled with high traveling & conveyance charges incurred during the year. Administrative expenses multiplied by 13.54 percent in 2024 due to higher payroll expenses as a result of inflationary pressure. The company squeezed its workforce from 320 employees in 2023 to 307 employees in 2024. Net other income posted a tremendous growth of 489.75 percent in 2024 unlike last year; the company didn’t book any provisioning for WWF and WPPF and also didn’t incur any unrealized loss on re-measurement of its investments at FVTPL. Moreover, other income strengthened on the back of the reversal of provision booked for WWF, gain recognized on the disposal of investments as well as higher profit earned from bank deposits. Despite handsome other income, HRPL posted an operating loss of Rs.36.29 million in 2024. Finance costs inched up by 1.35 percent in 2024 due to higher bank charges & commissions incurred during the year. Conversely, the unwinding of finance cost on provision for GIDC which formed the largest proportion of HRPL’s finance cost, ticked down during the year. The company posted a net loss of Rs.92.43 million in 2024 with a loss per share of Rs.92.43.

Recent Performance (1QFY25)

FY25 doesn’t look optimistic for HRPL so far, as evident by its topline slipping by 28.66 percent in 1QFY25. The impact of the superfluous supply of cheap soybeans in the local market continued to negatively impact the company’s business during the period. During the period, India announced to release of its rice in the international market. This will ease the international prices of rice (raw material of HRPL), however, its full impact hasn’t yet materialized. HRPL’s gross profit slumped by 63.60 percent in 1QFY25 with GP margin sliding down from 2.02 percent in 1QFY24 to 1.03 percent in 1QFY25. This was the consequence of thinner sales volume, higher utility charges, and lower export margins due to the stability of the local Rupee. The company also couldn’t pass on the impact of cost hikes in the local market due to lesser demand. Lower sales volumes as well as a curtailed advertising & promotion budget resulted in a 16.39 percent dip in HRPL’s distribution expense in 1QFY25. Conversely, administrative expense ticked up by 5.75 percent in 1QFY25 owing to inflationary pressure. The company didn’t incur any other expense during 1QFY25 due to no provisioning booked for WWF and WPPF. Other income also massively declined to the tune of 90.48 percent in 1QFY25. The detailed financial statements are not yet published to comment on the underlying reason for the other income recorded during the period. HRPL’s operating loss magnified by 187.12 percent to clock in at Rs.51.32 million in 1QFY25. Finance cost tumbled by 8.42 percent in 1QFY25 probably due to lesser unwinding of finance cost on provision for GIDC. The company recorded a net loss of Rs.57.63 million in 1QFY25, up 117.70 percent year-on-year. Loss per share stood at Rs.1.44 versus a loss per share of Rs.0.66 recorded during the same period last year.

Future Outlook

The international brown rice syrup market is staggeringly growing on account of consumers’ rising inclination towards organic sweeteners. HRPL must capitalize on this opportunity and focus on export sales to earn better margins. The company has recently announced the incorporation of a wholly owned subsidiary in Sharjah Airport International Free Zone (SAIF) to capitalize on the export opportunities.

The ease of rice exports by India will prove to be beneficial for the company as it will lower the international prices of its core raw materials.

HRPL being at the tail end of the gas pipeline suffers from inconsistent gas supply which impedes its production The company is considering cogen (also known as combined heat and power) as a possible substitute for gas to ensure uninterrupted production operations in order to enhance its sales volume.

Read the full story at the Business Recorder - Latest News website.