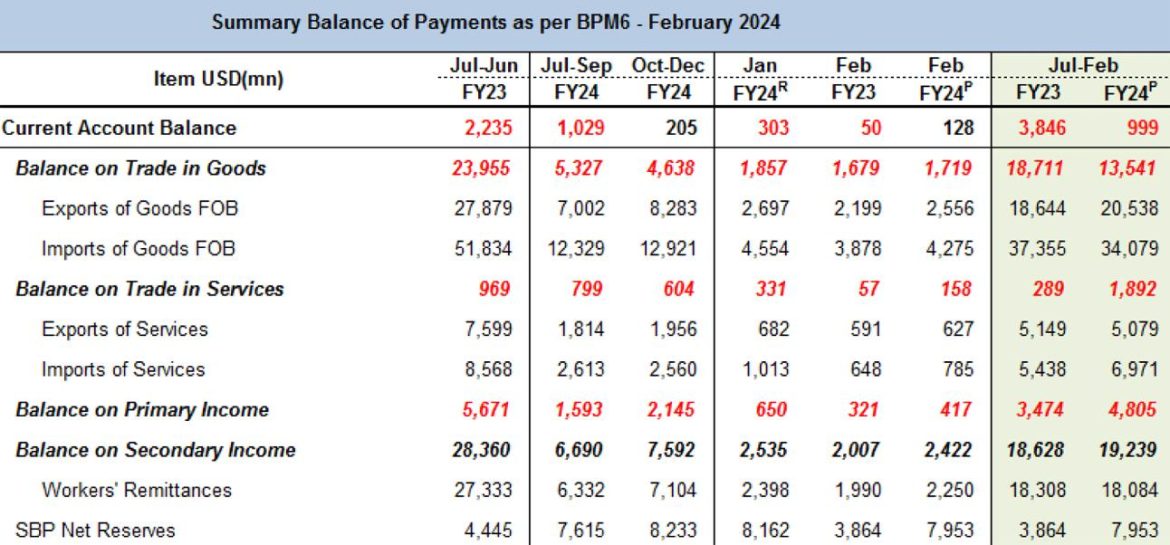

The practice of having near zero current account balance continues. In February 2024, the current account posted a marginal surplus of $128 million, and the 8MFY24 deficit stood at $999 million- down 74 percent compared to same period last year. The full year deficit is likely to remain below $2 billion.

The story is simple, and it has been recounted here multiple times. The import compression and demand destruction are real, and actual imports demand is lower than the restricted imports demand from last year. This situation is perhaps likely to prevail till the SBP reserves are built to a comfortable level, and till then the revival of economic growth and employment generation will remain a dream.

On the exports side, the performance in agriculture is better (food exports are up by 60 percent in 8MFY24 to $4.7billion),which is not letting the exports fall, and the economic growth this year is due to revival of agriculture sector.On the other side, textile and other manufacturing exports are falling mainly due to higher energy prices and record high interest rates.

Then there is a marginal decline in services exports and home remittances even though the number of people moving abroad is rising,while ICT (and freelance) export services are on a rise due to sluggish domestic economy and currency depreciation over the last two years. The dichotomy in the numbers and general trend is perhaps due to continued capital flight out of the country which is restricting the growth of formal remittances while service providers also tend to keep a chunk of their money abroad.

If the government seeks to instill investors’ confidence, and reduce the pace of capital flight,its only hope is home remittances and ICT exports, which can grow at a strong enough pace to result in a current account surplus, helping build SBP reserves, and allow the government to run policies for growth revival. Till then, zero CAD and near zero growth stimulus policies shall continue.

In 8MFY24, the imports (based on SBP data), are down by 9 percent to $34.1 billion. The decline is across the board barring machinery sector, where the backlog of machinery clearance and surging demand in mobile phones is keeping the imports growth in green.

However, in some sectors, the numbers are even lower than the restricted demand from last year. For example, in automobile good part of FY23, the CKD imports were capped at 50 percent of the imports in FY22, and so far in FY24, the demand is even lower – based on PBS data, transport imports in 8MFY24, is down by 23 percent from 8MFY23 and 62 percent from 8MFY22, to stand at mere $1.1 billion. And the cars production in 8MFY24 is down by 69 percent from 8MFY22.

The story of petroleum is not encouraging as well – the imports (SBP) in 8MFY24 is down by 21 percent from 8MFY23 to $10.0 billion. And quantity sales are down by 30 percent in 8MFY24 from the same period in the peak year (8MFY24). This is a significant dent in demand and the tale is not much different in many other sectors – such as chemicals and metals.

In exports, the lucky break is coming from rice exports which are keeping the growth high in food exports which is up by 60 percent to $4.7 billion in 8MFY24 on SBP data, and within it the rice exports are up by 78 percent to $2.4 billion. The rice bonanza is mainly due to export ban from India which has given Pakistan a windfall. Nonetheless, food exports, barring rice, are up 45 percent in 8MFY24, as currency depreciation, and better crops are doing the magic.

The concern is in textile and other manufacturing exports which have dipped, and the prospects are not very encouraging going forward, as high energy prices have caused low value-added textile (spinning and weaving) uncompetitive, and the energy prices are likely to increase further in the next fiscal year. Moreover, high interest rates are making life not easier as well. No amount of currency depreciation would be enough to solve the energy puzzles, as energy prices are linked to dollars. Thus, to boost textile and other manufacturing exports, the energy sector mess must first be solved, and circular debt ought to be controlled without further increase in the power prices.

The trend in services exports is encouraging, as IT exports are up by 15 percent to $2.0 billion in 8MFY24. The general trend is that more and more people are moving towards this sector, and freelancing is on the rise. However, not all exports are reflected in numbers, and similar is the story of remittances. The story of economic stability has to be sold to all, as some of the remittances and services exports are netted against the capital flight. If the capital flight stops, the inflows improve.

Thus, revival confidence is imperative if the current account and balance of payment situation is to improve meaningfully, enabling economic growth.

Read the full story at the Business Recorder - Latest News website.