Pakistan Synthetics Limited (PSX: PSYL) was incorporated in Pakistan as a private limited company in 1984 and was converted into a public limited company in 1987. The company is engaged in the manufacturing and sale of plastic caps, crown caps, Preform, PET Resin, and BOPET Resin.

Pattern of Shareholding

As of June 30, 2024, PSYL has a total of 138.699 million shares outstanding which are held by 1405 shareholders. Directors, CEO, and their spouses have the majority stake of 57.59 percent in the company followed by individuals holding 33.94 percent shares. Around 2.93 percent of shares of PSYL are held by mutual funds and 2.81 percent by NIT & ICP. The remaining ownership is distributed among other categories of shareholders.

Financial Performance (2019-24)

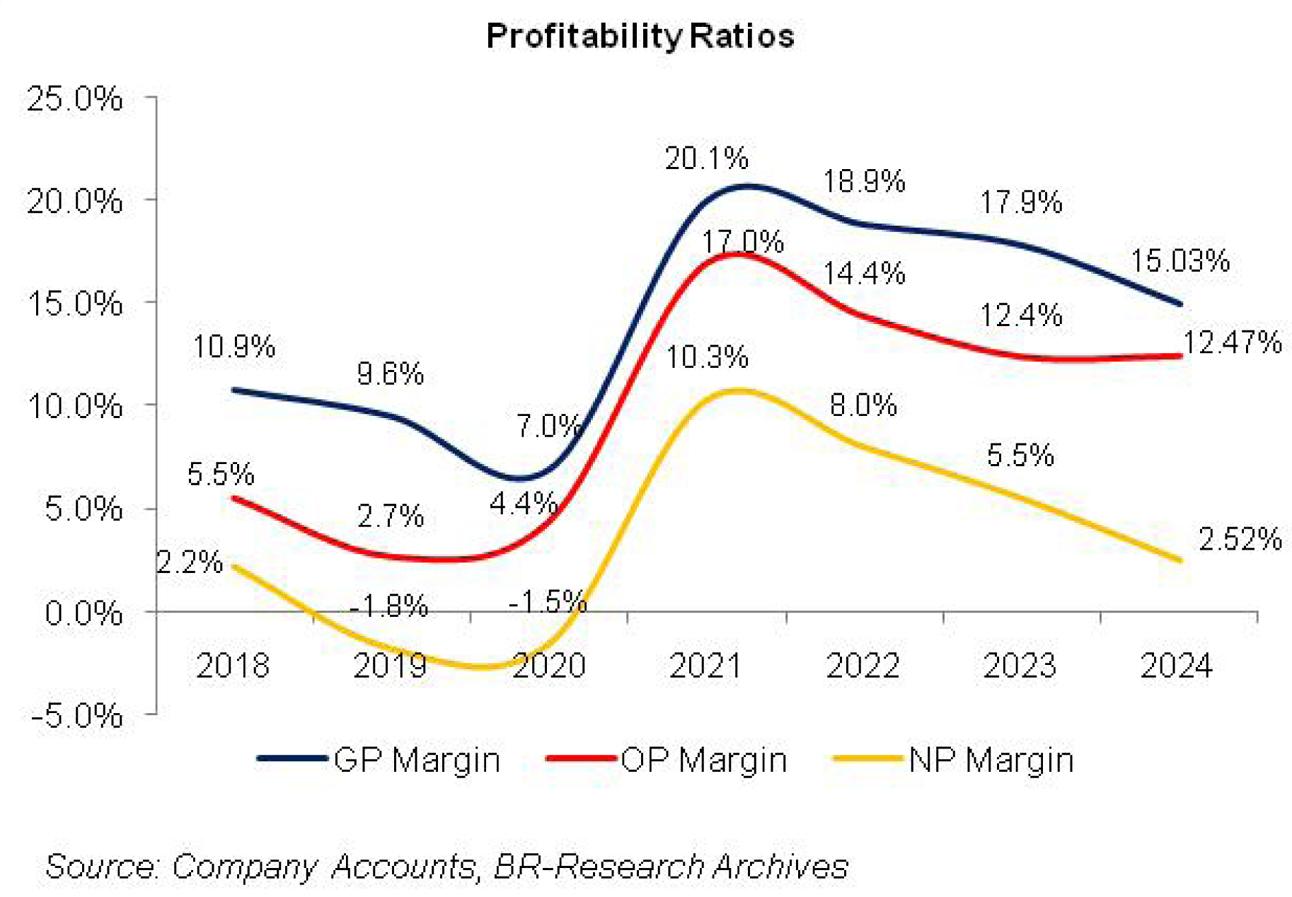

Barring year-on-year decline in 2020 and 2024, PSYL’s topline has been ascending in all the years under consideration. The company posted net losses in 2019 and 2020. In 2021, PSYL’s bottom line returned to profitability which further improved in 2022. However, it was followed by a bottom-line contraction in 2023 and 2024. PSYL’s gross margin followed a downhill journey until 2020, conversely, its operating margin dwindled in 2019 and then rebounded in 2020. In 2021, PSYL’s margins tremendously recovered only to tumble thereafter (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, PSYL’s net sales mounted by 33.74 percent year-on-year. This was on account of an encouraging rise in the sales volume of Resin. Moreover, the company instigated the PET Preform manufacturing plant in May 2018 and started the commercial sale of its output in 2019. The sales volume of plastic and crown caps slightly fell in 2019. The cost of sales hiked by 35.68 percent year-on-year in 2019 due to a 32 percent drop in the value of the Pak Rupee. Since PSYL imports nearly all of its raw materials, the declining value of local currency drastically inflated the company’s cost of doing business. Massive increases in gas prices also added to the ado. Gross profit grew by 17.85 percent year-on-year in 2019, however, GP margin slumped from 10.85 percent in 2018 to 9.56 percent in 2019. Operating expenses escalated by 11 percent year-on-year in 2019 due to an increase in payroll expenses as the number of employees rose from 306 in 2018 to 325 in 2019. Higher freight & handling charges, depreciation, and provision for ECL also contributed to higher operating expenses in 2019. Other expenses surged by an immense 102 percent in 2019 on account of exchange loss. This pushed the operating profit down by 35.68 percent year-on-year in 2019 with OP margin dipping to 2.7 percent from OP margin of 5.5 percent recorded in 2018. Finance costs magnified by 60.22 percent year-on-year in 2019 on the back of higher discount rates and increased borrowings. As a consequence, PSYL posted a net loss of Rs.123.90 million in 2019 as against a net profit of Rs.116.96 million posted in 2018. The company recorded a loss per share of Rs.2.18 in 2019 versus an EPS of Rs.2.09 registered in 2018.

PSYL’s net sales slumped by 6.23 percent year-on-year in 2020 owing to the outbreak of COVID-19 which considerably trimmed down the demand. There was a decline in the sales volume of Resin, crown caps, and plastic caps during the year. Conversely, the sales volume of Preform enhanced in 2020. During 2020, the prices of PET Resin in the international market significantly fell, resulting in heavy inventory loss for the company. This also squeezed the gross margin of PSYL which clocked in at 7 percent in 2020. Operating expenses spiked by 26 percent year-on-year in 2020 on account of a steep hike in freight and forwarding charges and elevated payroll expenses as the number of employees rose to 335 in 2020. Other expenses fell by 98.44 percent year-on-year in 2020 due to lower exchange loss. Other income rose by 21.61 percent year-on-year in 2020 on account of gain on disposal of fixed assets. Operating profit multiplied by 55.22 percent in 2020 with OP margin picking up to 4.4 percent. Finance costs surged by 18.41 percent in 2020 due to higher discount rates for most part of the year. PSYL registered a net loss of Rs.99.04 million in 2020, down 20 percent year-on-year. Loss per share was recorded at Rs.1.39 in 2020.

PSYL’s net sales rebounded by 10 percent in 2021. While the sales volume of Resin significantly fell in 2021, the off-take of Preform, plastic caps, and crown caps buttressed PSYL’s topline. Cost of sales slid by 5.38 percent year-on-year in 2021 due to favorable movement of local currency and prices of imported raw materials. Gross profit significantly rose by 215.62 percent in 2021 with GP margin jumping up to 20 percent. Operating expenses registered a 16.86 percent hike in 2021. Higher provisioning for WWF and WPPF drove other expenses up by over 1316 percent in 2021. Higher other expense was, to a great extent, offset by a 464.93 percent rise in other income on the back of exchange gain and net re-measurement gain on the provision of GIDC. In 2021, PSYL recorded 325.17 percent bigger operating profit compared to the previous year with OP margin climbing up to 17 percent. Monetary easing contributed towards lessening the finance cost by 51.33 percent in 2021. The company posted a net profit of Rs.748.37 million in 2021 with an NP margin of 10.32 percent and EPS of Rs.8.09, the highest among all the years under consideration.

In 2022, PSYL boasted the highest topline growth of 69.8 percent. This was on account of upward price revision and 25.5 percent growth in sales volume across categories. Radical depreciation of the Pak Rupee, high energy prices as well as escalated commodity prices particularly feedstock squeezed the gross margin to 18.87 percent in 2021. In absolute terms, gross profit grew by 59.83 percent in 2022. Operating expenses mounted by 61.69 percent in 2022 on account of higher sales volume which drove the freight and forwarding charges up. High fuel prices and elevated payroll expenses as the number of employees went up to 431 in 2022 from 369 in 2021 also had a say in driving up the operating expenses in 2022. Hefty exchange loss and profit-related provisioning inflated other expenses by 246 percent in 2022. As a consequence, operating profit marched up by 43.55 percent in 2022, however, OP margin slipped down to 14.38 percent. Increased borrowings and monetary tightening measures undertaken by the central bank in 2022 translated into 31.13 percent higher finance costs in 2022. Nevertheless, net profit ascended by 31.78 percent in 2022 to clock in at Rs.986.21 million with an NP margin of 8 percent. EPS dropped by 12 percent in 2022 to clock in at Rs.7.11 despite higher profitability. This was on account of the issue of 1 bonus share for every 10 shares held which increased the number of outstanding shares from 84.06 million in 2021 to 92.47 million in 2022.

PSYL’s net sales went up by 17.17 percent year-on-year in 2023. However, it was mainly driven by an increase in prices during the year. The cost of sales hiked by 18.62 percent in 2023 due to Pak Rupee depreciation and higher international commodity prices, particularly fuel. Gross profit enhanced by 10.95 percent in 2023; however, GP margin inched down to 17.87 percent. 50 percent higher operating expense in 2023 was the effect of higher fuel prices which drove up the freight and forwarding charges. Sales promotion, maintenance, and warranty expenses also hiked in 2023. Higher exchange loss pushed other expenses up by 33.83 percent year-on-year in 2023. Operating profit slumped by 0.84 percent year-on-year in 2023. OP margin ticked down to 12.17 percent in 2023. Finance costs escalated by 53.48 percent year-on-year due to high discount rate and increased borrowings. Net profit slid by 19.12 percent year-on-year in 2023 to clock in at Rs.797.68 million with EPS of Rs.5.75 and NP margin of 5.53 percent.

In 2024, PSYL’s net sales eroded by 4.34 percent. This was on account of a decline in sales volume due to political and economic instability and a decline in the purchasing power of consumers. High inflation and exorbitant energy and fuel prices didn’t allow the cost of sales to drop by a comparable proportion. This resulted in a 19.55 percent decline in gross profit in 2024 with GP margin falling down to 15 percent. Operating expense nosedived by 11.46 percent in 2024 mainly on account of thinner outward freight & handling charges due to lower sales volume. Other expenses declined by 87,39 percent in 2024 due to lower profit-related provisioning, no allowance booked for ECL and no exchange loss incurred during the year due to stable local currency. Other income strengthened by 247.27 percent in 2024 mainly on account of the reversal of the provision of ECL. Operating profit tumbled by 1.94 percent in 2024 with OP margin slightly picking up to clock in at 12.47 percent. Finance costs escalated by 121.43 percent in 2024 due to higher discount rates as well as increased short-term borrowings to meet working capital requirements. PSYL’s gearing ratio surged from 39 percent in 2023 to 52 percent in 2024. Share of loss on investment in associate company, Petpak Films (Private) Limited was recorded at Rs.318.92 million in 2024 versus share of loss of Rs.1.64 million recorded in 2023. PSYL recorded a net profit of Rs.347.765 million in 2024, down 56.4 percent year-on-year. This translated into EPS of Rs.2.51 and NP margin of 2.52 percent.

Recent Performance (1QFY25)

In 1QFY25, PSYL’s topline contracted by 3.31 percent due to demand destruction. The cost of sales also dipped by 3.85 percent due to stability in the value of the local currency. Gross profit declined by 0.415 percent in 1QFY25 with the GP margin clocking in at 16.19 percent portraying some improvement compared to the GP margin of 15.72 percent recorded in 1QFY24. Operating expense slumped by 10.87 percent in 1QFY25 probably on account of lower outward freight & forwarding charges incurred during the year. 55 percent year-on-year drop in other expenses during the period was due high-base effect as a hefty exchange loss was incurred in 1QFY24. Other income tumbled by 3.45 percent may be on account of the reversal of provisioning for ECL recorded during the previous year. Operating profit improved by 6.41 percent in 1QFY25 with OP margin recorded at 13.35 percent versus OP margin of 12.13 percent recorded during the same period last year. Finance cost inched up by 4.53 percent in 1QFY25 despite a downtick in the discount rate. This was due to increased short-term borrowings obtained during the year. PSYL also incurred a share of loss worth Rs.74.94 million on investment in associate in 1QFY25 which considerably diluted the net profit. Net profit was recorded at Rs.97.94 million in 1QFY25, down 31.92 percent year-on-year. This translated into EPS of Rs.0.71 in 1QFY25 versus EPS of Rs.1.04 recorded during the same period last year. NP margin also nosedived from 3.97 percent in 1QFY24 to 2.80 percent in 1QFY25.

Future Outlook

Exorbitant energy prices, elevated discount rates, and high general inflation for an extended time have brought industrial activity to a standstill, squeezing the demand for PSYL products. While recovery has been recorded in the economic parameters of late, the short-term to medium-term outlook remains uncertain due to the lingering effect of previous politico-economic instability. The company’s focus is to enhance its operational efficiency to sustain its margins and profitability.

Read the full story at the Business Recorder - Latest News website.