Smack in the middle of all the chest thumping around Pakistan achieving macroeconomic “stability”, power generation numbers have thrown a dampener. August 2024 electricity generation numbers from the national grid reads the problem statement loud and clear. Hard facts first. At 12.7 billion net units generated, this is the lowest August value in seven years. There has only been one previous incidence of the monthly year-on-year drop being higher than August’s 17.5 percent in eight years.

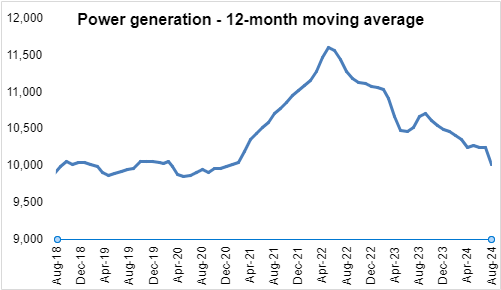

Mind you, August has historically received the highest power generation of all months – but that has all changed, and drastically. The only previous instance of August generation being lower than July only showed a deviation of less than 2 percent. The weather patterns from last year largely stayed unchanged in 2024. The fall is so steep that August 2024 generation is even lower than that of June of the year – which is well and truly unprecedented. The 12-month moving average power generation at 10 billion units is the lowest in forty-one months. The 2MFY25 generation is down 9 percent from the same period last year and the lowest 2-month number since FY19.

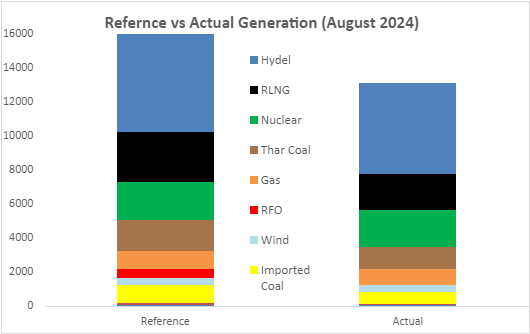

The reference power generation for 2MFY25 is slated at 30.9 billion units in the Power Purchase Price (PPP) used for reference the base tariff. The actual generation at 27.1 billion net units should worry authorities in Islamabad. Not that the monthly Fuel Charges Adjustment (FCA) has gone out of hand – in fact for the second month running, CPPA has requested a slight negative adjustment from reference fuel charges. That said the reference fuel charges are significantly higher than a year ago.

It is the periodic quarterly adjustments that could go for a spin one more time. Last year, it was largely the faulty assumptions in the PPP as regards the power generation mix that led to significantly higher monthly adjustments. This time around, that has been taken care of – as base tariff revision stands on more realistic grounds. While there may be little deviation in terms of generation mix – the dip in absolute generation is going to have a big impact as capacity charge component is going to balloon in unit terms.

The system’s nameplate and dependable generation capacity in the meanwhile, has grown substantially. Yes, the purchasing power of all consumer categories from domestic to industrial and from commercial to agriculture have significantly eroded in the recent past – life has not really come to a standstill for the system to return values from six and seven years ago.

Bloomberg puts Pakistan’s solar panel imports in the first six months of 2024 exceeding 13 gigawatts – more than double from a year ago – and four times form two years ago. Read it with a rather lucrative net metering policy for rooftop solar – and you have a simple explanation for where all the grid demand has evaporated. And this could just be the beginning as all the imported solar panels may not yet be reflected in the demand pattern. There are incentives to move away for those who can afford, and there are subsidies for those at the other extreme. There are not enough cushions for those stuck in the middle – and the situation will keep getting tougher, as more solar panels get erected. The single buyer model will ensure the capacity payments will have to be charged to whoever else is stuck with the grid.

Read the full story at the Business Recorder - Latest News website.